Safeguarding Your Assets: The Definitive 2026 Expat Guide to HUG Jeonse Deposit Insurance

The Architecture of Domestic Confidence

In the high-stakes theater of Seoul real estate, where the Jeonse system remains a fascinating yet formidable cultural phenomenon, the pursuit of domestic tranquility requires more than just aesthetic curation. As we navigate the complexities of 2026, the discerning urbanite recognizes that a residence is not merely a collection of curated furniture but a financial stronghold. The HUG Jeonse Deposit Insurance stands as the definitive arbiter of this security, transforming a potential liability into a protected asset.

The Essential Shield for Your Urban Sanctuary

The Korean Jeonse model—a unique structure of lump-sum deposits—demands a sophisticated hedging strategy. To inhabit a space with true poise, one must understand that the state-backed guarantee is the ultimate secondary guarantor. Should a landlord encounter financial turbulence or structural insolvency, the Corporation intervenes, ensuring the return of your capital. This is the bedrock of a refined lifestyle; ensuring your sanctuary remains untainted by market volatility. However, not every property qualifies for this elite protection; the property must be free from legal encumbrances and meet strict valuation criteria set for the 2026 market.

The Cost of Inviolable Security

A true connoisseur understands that peace of mind is an investment, never a mere expense. For the 2026 fiscal year, the insurance premiums represent a calculated allocation of resources. With rates fluctuating between 0.097 percent and 0.211 percent based on the property type and debt profile, the financial commitment is negligible compared to the magnitude of the deposit at stake. For a standard luxury apartment with a deposit of 300 million KRW, the estimated cost for a two-year contract—approximately 640,000 KRW—is the premium one pays for absolute autonomy and capital preservation.

| Property Type | Debt Ratio (LTV) | Annual Fee Rate |

|---|---|---|

| Apartment | Below 90% | 0.115% - 0.128% |

| Officetel / Villa | Below 90% | 0.139% - 0.154% |

| Multi-unit Housing | Varies | Up to 0.211% |

Strategic deductions are available for those who navigate the system with precision. Socially prioritized demographics—newlyweds, multi-child families, and those maintaining an impeccable fiscal record—may find their premiums reduced by up to 60 percent. Furthermore, the adoption of electronic contracts serves not only modern efficiency but also as a conduit for further fiscal optimization, streamlining the acquisition of your guarantee.

The Digital Pilgrimage to Protection

The application ritual has been modernized into a seamless digital experience for the 2026 resident. The elite urbanite no longer needs to endure the mundane queues of traditional bureaucracy. Platforms like Naver Pay and Kakao Pay, alongside the specialized HUG Ansim app, offer an intuitive gateway to security. For those who still value the tactile assurance of a physical institution, the grand halls of major commercial banks like Shinhan or KB Kookmin remain at your service. Timing is the most critical variable: one must initiate this process after the resident registration is perfected, yet before the midpoint of the lease term has elapsed.

Curating Your Documentation Dossier

Securing approval requires the assembly of a precise dossier. Each document must be freshly issued within the preceding month to ensure its institutional validity and clinical precision.

| Document Name | Purpose |

|---|---|

| Lease Agreement | Must include the Fixed Date (Hwak-jeong-il-ja) stamp. |

| Resident Registration | Proof of residency and priority rights (Deung-bon). |

| Payment Proof | Bank transfer records for the entire deposit amount. |

| Property Registry | Certified copy of the building registry (Deung-gi-bu-deung-bon). |

The Geometry of Value: The 126 Percent Mandate

A pivotal shift in regulatory policy, often referred to as the 126 percent rule, dictates the ceiling of insurable deposits. This calculation—derived from taking 90 percent of 140 percent of the government's appraised value—is the ultimate metric of property health. For those acquiring leases in modern villas or boutique officetels, verifying this ratio before any capital transfer is the difference between being fully protected and being left vulnerable to the whims of the market.

The Art of the Protected Contract

A discerning tenant knows that the lease is a living document. Engaging professional accompaniment during the signing ceremony ensures that the landlord's fiscal transparency is absolute. A vital inclusion—and a hallmark of the sophisticated tenant—is the clause that nullifies the agreement and mandates an immediate refund should the insurance be denied due to reasons attributable to the property. This is the ultimate failsafe for the modern expatriate navigating the Korean landscape.

Timing Your Financial Shield

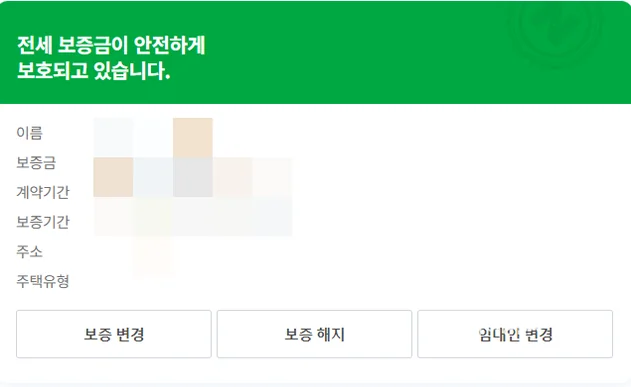

The ideal window to finalize your insurance is within the inaugural week of your residency. Once you have orchestrated your move and updated your address at the community center, the legal perfection of your tenancy is established. In 2026, administrative efficiency is at its zenith, and most digital applications are processed within a fortnight, providing you with a certificate of guarantee that acts as an impenetrable financial shield.

Director K's Final Assessment & Global Inquiry

Investing in your domestic security is as vital as the geography of your home. The HUG Jeonse Deposit Insurance is the quintessential tool for global citizens to navigate the Korean market with the confidence of a local. By adhering to the 126 percent mandate and utilizing sophisticated digital platforms, you ensure that your tenure in Korea is defined by luxury and tranquility rather than financial anxiety.

Is this institutional protection mandatory?

While optional for most private tenancies, it is a non-negotiable recommendation for the prudent. However, for properties under registered rental businesses, the landlord is legally compelled to enroll and share the financial burden of the fee with the tenant.

Does the landlord's nationality affect eligibility?

The system remains inclusive. As long as the property is situated within the Korean territory and aligns with HUG criteria, the landlord's nationality does not disqualify the tenant from this tangible legacy of protection.

What are the protocols for contract renewal?

Upon the extension of a lease, a renewal of the insurance policy is required to mirror the new temporal boundaries. One must ensure the deposit remains within the current year's valuation ratios to maintain continuous coverage.

📅 Local Weather Guide

Seoul Weather🌐 Read this post in other languages:

• 🇯🇵 日本語版 (Japanese Version)

Join the conversation